The

Attorney General of Mississippi has filed a lawsuit against Experian,

which, along with Transunion and Equifax, make up the three largest

credit reporting companies. These companies collect information about

consumers and then sell it back to lenders, insurance companies and

others. The problem is that these reports on consumers are frequently

full of mistakes and misinformation. According to investigators with the

Mississippi Attorney General's office, Experian mixed up reports of

consumers with the same or a similar name, reported inaccurate

information and then failed to remove it when told of the error and

failed to investigate potential mistakes despite warnings from consumers

that an error existed.

The Mississippi Attorney General's allegations aren't the first time these problems have been identified. The Federal Trade Commission says 5% of consumers, or 10 million people have credit report errors so significant that they have impacted the consumer's credit. The investigators also found former employees of Experian who said they were pressured to meet certain quotas for the cases and to keep any investigations and phone calls with consumers short. If you've found an error in information contained in your credit reports please contact us to discuss the next steps in resolving the issues. |

||

Thursday, July 3, 2014

CREDIT REPORT MISTAKES

Tuesday, May 27, 2014

IS THIS DEBT YOURS?

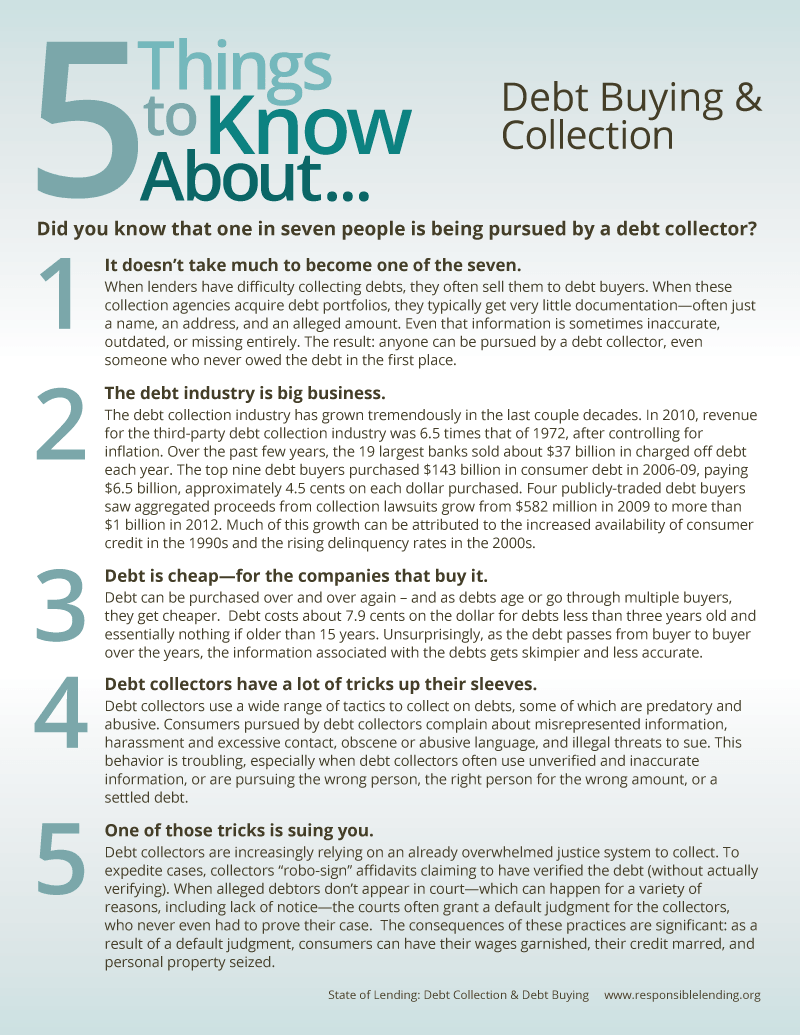

According to the Federal Reserve, one in seven Americans is being contacted by a debt collector.

This is up from one in twelve just ten years ago. With 4,500 debt

collection agencies in the United States, people find it hard to keep

track of who is collecting which debt. Debts are bought and sold so many

times that in the bankruptcy schedules we prepare we often list

multiple debt collection agencies for one debt just to try to make sure

we've hit upon the current owner. Between 2006-2009 the top nine debt

buyers purchased 90 million accounts to collect. While most of the debt

sold is credit card accounts, other debts like medical bills and

utilities are increasingly bought and sold. Experts believe other debts

such as cell phone bills, auto loan deficiencies and student loans will

be increasingly part of a debt buyer's portfolio.

This frequent buying and selling of debt creates other problems for legitimate debt collection too. For example, old debt is usually sold for pennies on the dollar and at such low prices original creditors have no incentive to try to provide the debt buyer with any loan documents like credit applications or account statements. As a result, debtors can be sued by a debt buyer with none of the evidence that would typically be required to prove that the agency suing is actually the owner of the debt. Debt collection agencies have also been known to use false affidavits, sue the wrong person, sue on debt beyond the statute of limitations, sue on debt discharged in bankruptcy and sue on debt that's already been paid. In some cases debt buyers just find people with the same or a similar name to sue, regardless of whether the person is actually the one who incurred the debt. In other cases, employees of the debt buyers engage in "robo-signing" of affidavits where they machine stamp their name to thousands of affidavits in a single day, despite the requirement that the affidavit be signed only after the person has personally reviewed and verified the accuracy of the the information. And since the defendants in nearly all debt collection lawsuits don't do anything to challenge the legitimacy of the claims, debt collectors are winning record numbers of lawsuits, resulting in garnishment of wages and bank accounts. If you live in Polk County and are facing debt collection we are willing to discuss defending these debt collection lawsuits on a flat fee basis. Contact us immediately after a debt collection agency contacts you so we can discuss your options. |

||

|

.

|

Wednesday, April 23, 2014

COLORADO SUES DEBT BUYER

|

Monday, March 10, 2014

ESCAPING THE DEBT MACHINE

Over one billion contacts are made

each year by debt collectors to consumers and the contingency fees raked

in by third party debt collectors exceeds many billions of dollars. The largest debt collector, NCO Financial which is owned by JPMorgan Chase, earns nearly $2 billion annually. A report from the National Consumer Law Center (NCLC) called

The Debt Machine: How the Collection Industry Hounds Consumers and Overwhelms Courts, describes both the enormous profits in the debt collection industry and also the flaws in the legal system. For example, despite debt collectors rarely having the documentation necessary to prove their claims in court or failing to properly serve debtors or suing on debts beyond the statute of limitations, judges

in Iowa estimate 85% to 90% of all collection lawsuits result in a

default judgment because the consumer defendant does nothing to defend

against the lawsuit.

Some debt collectors specialize in collecting debts that are uncollectible. A debt collector in Minnesota, for instance, focuses exclusively on collecting debts from dead people and Portfolio Recovery Associates has admitted continuing to earn fees on debts well beyond the statute of limitations. With consumers usually doing nothing to defend against debt collection lawsuits, collectors can pay as low as pennies on the dollar and still earn billions of dollars in revenue collecting these debts. The NCLC report also documents how some debt collectors trick consumers into making a partial payment or offering so-callled "zombie cards" that "allow" them to make payments on debt owed using a credit card. Unwittingly, these partial payments result in an acknowledgment of the debt that restarts the clock on the statute of limitations. If you're facing debt collection on an old debt or one brought by a debt collector other than the original creditor don't just let a default judgment be entered. Contact us immediately after being served with the lawsuit to determine if there are defenses. |

Wednesday, February 19, 2014

PAYDAY LOAN COMPANY ON RESERVATION SUBJECT TO IOWA LAW

An important September 2013 ruling from the Iowa Department of Inspections and Appeals said that Western Sky Financial, an Internet payday loan company owned by a member of the Cheyenne River Sioux Tribe and located on the Cheyenne River Sioux reservation in South Dakota is subject to Iowa consumer laws. Western Sky sells the loans it makes to WS Funding, a subsidiary of CashCall, which services all the loans made in Iowa by Western Sky. The payday loans made by Western Sky can carry interest rates in excess of 135%. Western Sky and CashCall had argued that since it was owned by a tribal member and located on a reservation it was entitled to sovereign immunity and not subject to Iowa state laws. The Administrative Law Judge ruled, however, that since Western Sky was not the Tribe itself and most of the transactions occurred off the reservation, Iowa laws controlled. The judge said that since Western Sky solicited Iowa consumers to enter into loan agreements via the Internet it couldn't hide behind tribal sovereign immunity to shield itself from Iowa laws. If you're having problems with Western Sky or another payday loan company connected with a tribe contact us about what might be done. |

||

Friday, December 6, 2013

DEBT COLLECTION COMPLAINTS INCREASING

Consumer complaints about debt

collection activities have increased significantly. Between 1999 and

2009, complaints to the Federal Trade Commision about collection

agencies, debt buyers, collection attorneys and mortgage servicers

increased from 10,000 to almost 90,000. The growth in the "debt buying"

industry has led to many of these new complaints. Each year creditors

write off hundreds of billions of dollars in debt that they believe to

be uncollectible. But for the consumers who owe the debt the story

doesn't end there. For pennies on the dollar "debt buyers" will purchase debt to try collection of their own. Using automated robocalls, lawsuits and other tactics debt buyers work to collect debt that might be several years old.

Fortunately for the consumers facing these debt collection activities there are several options. First, there might be defenses to a debt collection lawuit such as the statute of limitations or a lack of evidence that the debt is owed. Most debt collection lawuits aren't opposed by consumers and debt buyers count on no opposition so they can obtain default judgments. Raising defenses to these lawsuits might result in dismissal. Second, consumers can go on the offensive by bringing an action against debt buyers for violation of federal and state debt collection laws. Debt buyers who engage in illegal debt collection activity like robocalls to cell phones without permission, harassment, calls to third parties and many other actions can be liable for damages and attorney fees. Third, if the amount of debt is significant, bankruptcy can be filed to discharge the debt while also preserving a consumer's right to bring a fair debt collection lawuit against the debt collector. If you're facing debt collection contact us as soon as possible to discuss your options. |

Wednesday, November 13, 2013

SPECIALTY CONSUMER REPORTING AGENCIES COVERED BY FCRA

|

||

|

|

Subscribe to:

Comments (Atom)